Have you ever gotten a raise and felt excited about all the extra money you’d be able to save, only to find your bank account balance looks exactly the same a year later? You aren’t alone. In fact, you might be experiencing a very common financial phenomenon known as lifestyle inflation.

It’s easy to assume that more income automatically equals more wealth. However, for many Americans, earning more often leads to spending more. As paychecks grow, so do expectations for comfort, convenience, and luxury. Before you know it, that “extra” money has been absorbed by a nicer car, a bigger apartment, or more frequent takeout orders.

This cycle can be dangerous for your long-term financial health. While enjoying the fruits of your labor is important, unchecked spending can derail retirement plans and prevent you from building a safety net. In this guide, we will explore exactly how lifestyle inflation affects savings in the USA, why it happens, and actionable steps you can take to stop it in its tracks.

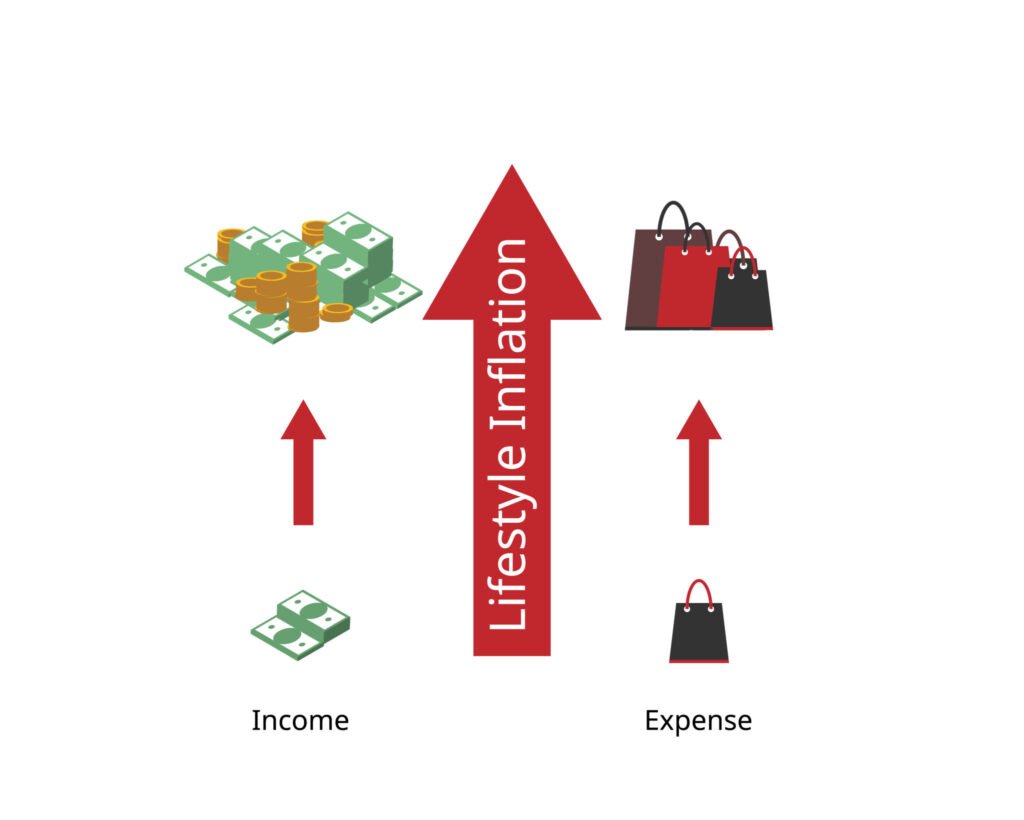

What Is Lifestyle Inflation?

Lifestyle inflation—often referred to as lifestyle creep—occurs when an individual’s spending increases in proportion to their income. It’s the subtle shift from treating yourself occasionally to upgrading your entire standard of living permanently.

Lifestyle inflation meaning

At its core, lifestyle inflation means that as you earn more, things that were once considered luxuries become necessities. When you were a college student, a shared apartment and instant noodles might have been acceptable. As a young professional, you might upgrade to a studio and casual dining. As you advance in your career, you might feel that you “need” a luxury vehicle or a house with a guest room you rarely use.

How spending grows with income

The process is often gradual. It starts with small choices: buying brand-name groceries instead of generic, subscribing to premium streaming services without ads, or opting for the newest smartphone model. Because the increases are incremental, they often go unnoticed until the monthly credit card bill arrives. This phenomenon explains why someone earning $100,000 a year may live paycheck to paycheck just like someone earning $40,000.

Why lifestyle inflation is common in the USA

In the United States, consumer culture plays a massive role. We are constantly bombarded with advertisements suggesting that success looks a certain way. From social media influencers flaunting vacations to neighbors buying new cars, the pressure to “keep up” is immense. Combined with easy access to credit, lifestyle inflation in the USA is almost the default mode for many households unless they actively choose otherwise.

Why Lifestyle Inflation Is a Problem for Savings

The most significant danger of lifestyle creep isn’t just that you spend more; it’s that you save less relative to what you earn.

Higher income doesn’t guarantee higher savings

A common misconception is that saving money becomes effortless once you reach a certain income bracket. Data suggests otherwise. If your expenses rise in lockstep with your salary, your savings rate remains stagnant. You might be earning double what you did five years ago, but if your spending has also doubled, you are no closer to financial freedom.

Reduced ability to build emergency funds

When your baseline expenses are high, you need a larger emergency fund to feel secure. If you spend $3,000 a month, a three-month emergency fund is $9,000. If lifestyle inflation pushes your monthly spend to $6,000, you now need $18,000 just to have the same level of security. Unfortunately, because the extra income is being spent, that larger safety net rarely gets built, leaving high earners surprisingly vulnerable to job loss or medical emergencies.

Long-term impact on wealth creation

Wealth is built on the gap between income and expenses. Lifestyle inflation closes that gap. Every dollar spent on an unnecessary upgrade is a dollar that isn’t compounding in an investment account. Over 10, 20, or 30 years, the opportunity cost of saving money in the USA is massive. That missed investment growth can mean the difference between retiring early and working well into your 70s.

Common Examples of Lifestyle Inflation in the USA

Recognizing lifestyle creep is the first step to stopping it. Here are some of the most common ways spending habits in the USA shift as income rises.

Housing upgrades and rent creep

Housing is typically the largest expense for Americans. When people get a raise, their first instinct is often to move to a “nicer” neighborhood or a bigger apartment. While a safe and comfortable home is essential, upgrading from a perfectly adequate $1,500 apartment to a $2,500 one simply because you can afford it is a classic example of lifestyle inflation.

Frequent dining out and food delivery

Food spending is a sneaky budget killer. It evolves from cooking at home to grabbing fast casual lunches, then to frequent dinners at sit-down restaurants. Food delivery apps have accelerated this trend, adding delivery fees and tips to the cost of a meal that would have been a fraction of the price if cooked at home.

Car upgrades and subscription overload

The “new car smell” is expensive. Upgrading a reliable vehicle for a luxury model with a higher monthly payment, premium gas requirement, and higher insurance premiums is a major wealth destroyer. Similarly, subscription overload—paying for five different streaming services, a monthly clothing box, and a premium gym membership you don’t use—eats away at disposable income silently.

How Lifestyle Inflation Affects Long-Term Financial Goals

The consequences of lifestyle inflation extend far beyond monthly cash flow; they jeopardize your future.

Retirement savings impact

Lifestyle inflation and retirement are fundamentally at odds. If you grow accustomed to living on $100,000 a year, you will need a massive portfolio to support that same lifestyle in retirement. If you had kept your living expenses at $60,000, your retirement number would be significantly lower and easier to achieve. By inflating your lifestyle, you are essentially moving the finish line further away while simultaneously running slower.

Delayed homeownership

For many, owning a home is a key part of the American Dream. However, lifestyle creep can delay this goal significantly. Money that could have gone toward a down payment is instead diverted to rent for a luxury apartment or lease payments for a luxury car. This delay can cost buyers years of potential equity growth.

Increased reliance on debt

Ironically, earning more can sometimes lead to more debt. As people feel wealthier, they may feel more comfortable taking on leverage. They might put a vacation on a credit card assuming their next bonus will cover it, or take out a large loan for a boat. This increased reliance on debt creates a fragile financial foundation where a single disruption in income can cause the whole structure to collapse.

Psychological Reasons Behind Lifestyle Inflation

Understanding the psychology behind spending behavior in the USA is crucial for changing it. It’s not just about math; it’s about mindset.

Social comparison and peer pressure

Humans are social creatures. We naturally compare ourselves to our peers. If your friends are buying houses, traveling to Europe, and wearing designer clothes, you feel a subconscious pressure to do the same to fit in. This “keeping up with the Joneses” mentality drives much of the lifestyle creep psychology we see today.

“I deserve it” mindset

Work can be stressful. After a long week or a grueling project, it’s easy to justify a purchase by saying, “I worked hard for this; I deserve it.” While treating yourself is healthy, using spending as a primary reward mechanism creates a direct link between stress and spending, which can be hard to break.

Lifestyle creep through convenience spending

As you earn more, you often have less free time. This leads to spending money to buy time or convenience—hiring house cleaners, ordering delivery, or taking Ubers instead of public transit. While some of these trade-offs make sense, they often accumulate without conscious decision-making, leading to a bloated budget.

Lifestyle Inflation vs Cost of Living Increases

It is important to distinguish between voluntary lifestyle inflation and unavoidable economic factors.

Key differences explained

Lifestyle inflation is a choice: buying a Tesla when your Honda Civic works fine. Cost of living increases are external: your landlord raising the rent, gas prices spiking, or the price of eggs doubling due to inflation. One is within your control; the other is not.

When higher spending is unavoidable

Sometimes, spending increases because life stages change. Getting married, having children, or caring for aging parents will naturally increase your expenses. This isn’t necessarily lifestyle inflation; it’s life. However, even within these categories, there is room for choice (e.g., buying brand-new baby gear vs. gently used).

How to adjust budgets smartly

When facing cost of living increases vs lifestyle inflation, the strategy differs. For cost of living hikes, you may need to negotiate bills or cut discretionary spending. For lifestyle inflation, the solution is self-discipline. Understanding the difference prevents you from feeling helpless against rising costs and empowers you to control what you can.

How to Avoid Lifestyle Inflation and Save More

You don’t have to live like a pauper to avoid lifestyle creep. You just need a plan.

Automate savings and investments

The most effective way to avoid lifestyle inflation is to pay yourself first. Set up automatic transfers to your savings or investment accounts to occur on payday. If the money never hits your checking account, you can’t spend it. When you get a raise, immediately increase your automatic transfer amount so your checking account balance stays roughly the same.

Increase savings rate with income raises

A great rule of thumb is to save at least 50% of every raise or bonus. If you get a $5,000 raise, put $2,500 directly into investments and use the other $2,500 to enjoy life. This allows you to increase savings in the USA while still feeling the reward of your hard work.

Practice mindful spending

Before making a purchase, pause. Ask yourself if this upgrade will truly add value to your life or if it’s just a fleeting desire. Mindful spending isn’t about restriction; it’s about aligning your spending with your values. If travel is important to you, spend there—but cut back ruthlessly on things that don’t matter, like cable TV or expensive clothes.

Smart Habits to Control Lifestyle Inflation

Building wealth is a habit, not an event. Here are actionable personal finance habits to adopt.

Budgeting with intent

A budget shouldn’t be a constraint; it should be a roadmap. Zero-based budgeting, where every dollar is assigned a job, is particularly effective. By deciding in advance how much goes to “fun” money, you can spend guilt-free without compromising your savings goals.

Delaying gratification

Implement a “72-hour rule” for large purchases. If you see something you want, wait three days. Often, the urge to buy will fade. This simple habit prevents impulse purchases that fuel lifestyle inflation.

Tracking expenses regularly

You can’t manage what you don’t measure. Use apps or spreadsheets to track your spending habits in the USA. Seeing a visual representation of how much you spend on dining out or subscriptions can be a sobering wake-up call that prompts immediate behavioral change.

Common Mistakes People Make With Lifestyle Inflation

Even the most financially savvy individuals can fall into traps.

Upgrading everything at once

The biggest mistake is the “domino effect” of upgrades. You get a new house, so you buy new furniture, which makes your old TV look small, so you buy a new TV. Try to space out upgrades rather than doing them all simultaneously.

Ignoring small recurring expenses

People often focus on the big ticket items and ignore the $15 monthly subscriptions. But ten $15 subscriptions equal $1,800 a year. These small leaks can sink a large ship.

Not revisiting financial goals

As your income grows, your goals should evolve. If you aren’t regularly reviewing your personal finance goals, your spending will naturally expand to fill the void. Set clear targets for net worth, retirement contributions, or debt payoff to keep your focus sharp.

Frequently Asked Questions (FAQ)

Is lifestyle inflation always bad?

Not necessarily. There is a healthy level of lifestyle inflation. Moving from an unsafe neighborhood to a safe one, or buying healthier food, are positive changes. The problem arises when spending compromises your financial security and future goals.

How much should savings increase with income?

Ideally, your savings rate (the percentage of income you save) should increase as your income rises. Since your basic needs are met, a larger portion of every additional dollar should go toward savings. Aiming to save 20-25% of your gross income is a strong benchmark for high earners.

Can lifestyle inflation affect high earners too?

Absolutely. In fact, high earners are often the most susceptible. The pressure to maintain a “wealthy” image can lead to living paycheck to paycheck on a six-figure salary. Income level does not protect you from poor spending habits.

What is the easiest way to control lifestyle inflation?

The easiest first step is to “hide” your money from yourself. Use automated contributions to 401(k)s and IRAs so the money is invested before you even see it.

How can couples manage lifestyle inflation together?

Communication is key. Have regular “money dates” to discuss joint budgeting strategies. Agree on a threshold for purchases that require mutual discussion (e.g., anything over $200). Ensure you are both aligned on long-term goals so you aren’t working against each other.

Final Thoughts on Lifestyle Inflation and Savings

Earning more money should be a tool for liberation, not a shackle that binds you to higher monthly payments. Lifestyle inflation affects savings in the USA by turning potential wealth into temporary comfort.

Income growth should build freedom, not pressure. By remaining aware of lifestyle creep, automating your savings, and making intentional spending choices, you can break the cycle. Remember, true wealth isn’t about the car you drive or the clothes you wear—it’s about the security and options you build for your future.