Understanding Risk in Long-Term Investments in the USA

When most people hear the word “risk” in the context of money, they think of losing everything. They imagine a stock market crash where their savings evaporate overnight, or a bad bet that leaves them penniless. This fear keeps millions of Americans sitting on the sidelines, holding their savings in cash or low-interest accounts where they feel safe.

But in the world of long-term investing, the biggest danger isn’t necessarily the market going down temporarily. The bigger danger is often playing it too safe. If your money isn’t growing fast enough to keep up with the rising cost of living, you are slowly losing purchasing power every single year.

Understanding risk is the key to building wealth. It isn’t about avoiding danger entirely; it is about recognizing different types of danger and deciding which ones you are willing to accept in exchange for potential growth. Whether you are saving for retirement in a 401(k), building a college fund, or just trying to grow your net worth, learning to navigate risk is the most profitable skill you can develop.

What Is Investment Risk?

At its core, investment risk is the probability that an investment’s actual return will be different from what you expected. This includes the possibility of losing some or all of your original investment. However, risk is not a binary switch where something is either “safe” or “risky.” It exists on a spectrum.

It is important to distinguish between risk and uncertainty. Risk involves unknown outcomes where the probabilities can be estimated—like knowing that the stock market has historically returned about 10% annually on average, despite crashing occasionally. Uncertainty is when you don’t even know what the possible outcomes are. In investing, we generally deal with risk. We accept that asset prices will fluctuate in the short term in exchange for the likelihood of growth in the long term.

Why Risk Matters in Long-Term Investing

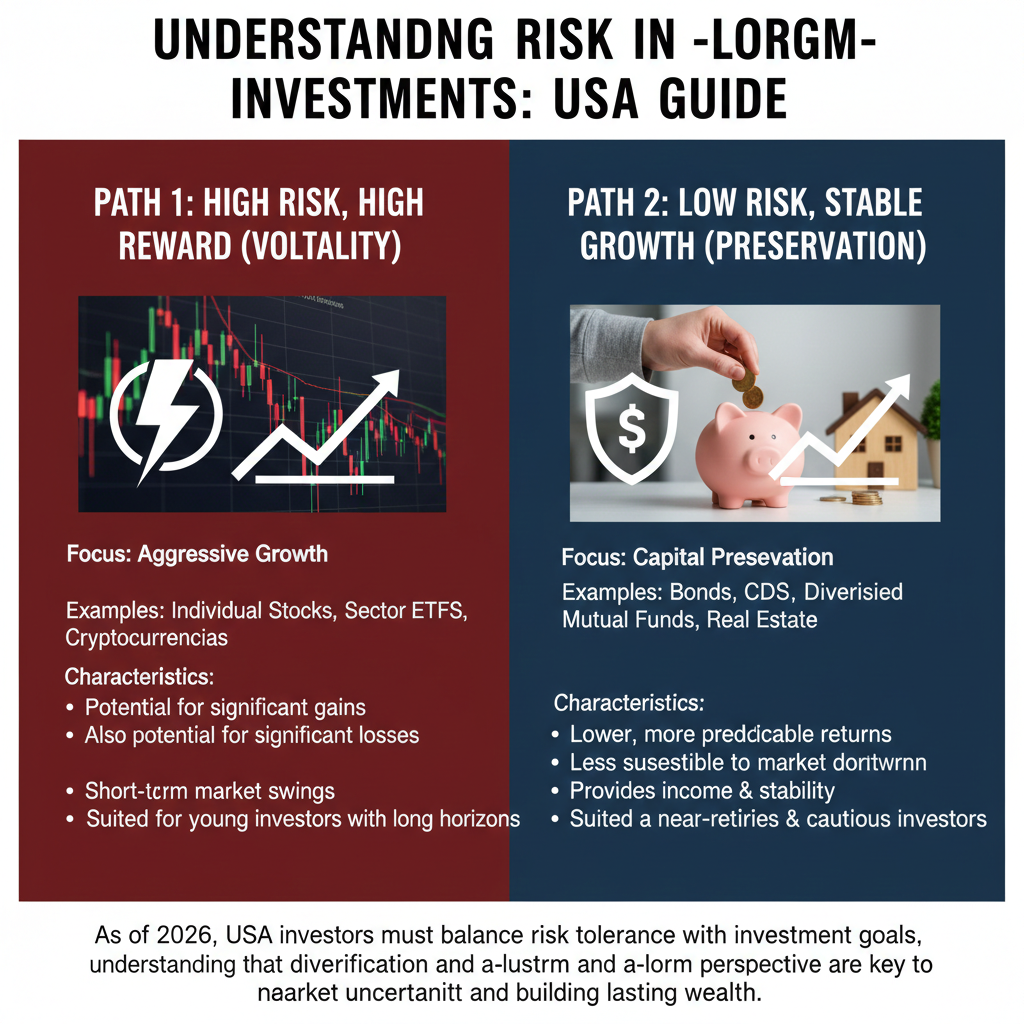

Risk and reward are two sides of the same coin. In the financial markets, you are generally paid for taking on risk. If an investment were perfectly safe and guaranteed to make a huge profit, everyone would buy it, driving the price up and the return down until it was no longer a “sure thing.”

To get higher returns, you generally have to accept more volatility (the ups and downs of price). If you want perfect safety, you generally have to accept lower returns.

This trade-off becomes critical when you consider inflation. Inflation is the rate at which the price of goods and services rises. If a savings account pays 4% interest but inflation is running at 3%, your “real” return is only 1%. If inflation jumps to 5%, that “safe” savings account is actually losing purchasing power. Taking on investment risk is the primary way to beat inflation and grow your wealth over decades.

Types of Investment Risk

Risk isn’t a single monster; it’s a collection of different challenges. Understanding the specific type of risk you are facing helps you manage it.

Market Risk

This is what most people think of first. Market risk (or systematic risk) is the chance that the entire market will decline, dragging your investments down with it. This can be caused by economic recessions, geopolitical events, or changes in interest rates. For example, during the 2008 financial crisis, almost all stocks dropped in value regardless of how well the individual companies were performing. You cannot eliminate market risk entirely if you want to participate in the market’s growth.

Inflation Risk

As mentioned earlier, this is the silent killer of wealth. Inflation risk is the danger that the money you make on your investment won’t be worth as much in the future as it is today. Historically, cash and bonds are most vulnerable to inflation risk, while stocks and real estate tend to hold up better because companies can raise prices and property values generally rise with inflation.

Interest Rate Risk

This primarily affects bond investors. There is an inverse relationship between interest rates and bond prices. When interest rates go up, the value of existing bonds goes down. If you hold a bond paying 3% and new bonds are issued paying 5%, nobody wants your 3% bond unless you sell it at a discount. If you need to sell that bond before it matures, you will lose money.

Credit and Default Risk

This is the risk that the borrower won’t pay you back. If you buy a bond from a company (corporate debt) or a government (municipal or treasury debt), you are lending them money. If that entity goes bankrupt or defaults, you could lose your investment. U.S. Treasury bonds are considered to have virtually zero default risk, while “junk bonds” from struggling companies have high default risk (and therefore pay higher interest rates).

Liquidity Risk

Liquidity refers to how quickly you can convert an investment into cash without losing value. Stocks in major companies like Apple or Microsoft are highly liquid—you can sell them instantly during market hours. A house is illiquid; it can take months to sell. If you have an emergency and need cash immediately, having all your money tied up in illiquid assets is a major risk.

Risk and Time Horizon

Your time horizon—how long you plan to hold an investment—is the single most important factor in determining how much risk you can handle.

Short-term investing (less than 3–5 years) is highly sensitive to volatility. If you are saving for a down payment on a house that you plan to buy next year, you cannot afford to put that money in the stock market. If the market drops 20% right before you need the money, your plans are ruined.

Long-term investing (10+ years) changes the equation. History shows that over long periods, the U.S. stock market trends upward. Time allows you to ride out the inevitable downturns. If the market crashes when you are 30 years old and retirement is 30 years away, you have plenty of time for your portfolio to recover and reach new highs. In fact, for a young investor who is consistently buying, a market crash is actually a buying opportunity (a sale) rather than a disaster.

Risk Tolerance vs. Risk Capacity

When determining your strategy, you must balance your emotional ability to handle loss with your financial ability to handle loss.

Risk Tolerance is emotional. It is how well you sleep at night when your portfolio value drops. Some investors panic when they see their account down 5%; others shrug it off knowing it will bounce back. If you have low risk tolerance, you might sell at the bottom of a crash out of fear, locking in losses.

Risk Capacity is financial. It is a measure of how much risk you can afford to take. A 25-year-old with a steady job and low expenses has a high risk capacity because they have time to recover. A retiree living off their portfolio has a low risk capacity because a major loss could impact their ability to pay for groceries.

It is common to have a mismatch here. You might have a high capacity for risk (young, high income) but a low tolerance (hate losing money). Successful investing involves finding a middle ground where you take enough risk to reach your goals without taking so much that you panic-sell.

How Diversification Reduces Risk

There is a famous saying in finance: “Diversification is the only free lunch.” It is the primary way investors manage risk without sacrificing too much return.

Diversification means spreading your money across different investments so that if one fails, it doesn’t sink your whole ship.

Asset Classes Explained

You don’t just buy different stocks; you buy different types of assets. When stocks are going down, bonds might be going up. When inflation is hurting your bonds, your real estate might be booming. By holding a mix of stocks, bonds, and cash, you smooth out the ride.

Domestic vs. International Exposure

Diversification also applies geographically. If the U.S. economy enters a recession, emerging markets or European markets might still be growing. A well-diversified portfolio usually includes exposure to international markets to capture growth wherever it happens.

Risk by Asset Type

Understanding the general risk profile of common assets helps you build a balanced portfolio.

- Stocks (Equities): High risk, high potential return. You own a piece of a company. If the company fails, you lose money. If it succeeds, you share in the profits. Over the long term, stocks have historically provided the best returns.

- Bonds (Fixed Income): Moderate to low risk, moderate returns. You are a lender. Government bonds are generally safer than corporate bonds. Bonds provide steady income and act as a shock absorber for your portfolio when stocks fall.

- Real Estate: Moderate to high risk. Real estate offers physical asset ownership and potential rental income. However, it requires maintenance, lacks liquidity, and is subject to local market conditions.

- Cash Equivalents (CDs, Money Market): Low risk, low return. These are safe places to park money for the short term. The principal is usually insured (by the FDIC in the US), but returns rarely beat inflation over the long haul.

Common Risk Myths in Investing

Misconceptions about risk often lead investors astray. Let’s debunk a few.

Myth: “Higher risk always means gambling.”

Gambling is wagering on an outcome where the house has the advantage (negative expected return). Investing is accepting volatility in a system that has historically grown (positive expected return). When you buy a broad stock market index fund, you are betting on human ingenuity and corporate growth, not a spin of a roulette wheel.

Myth: “Avoiding risk is safer.”

As discussed, keeping all your money in cash feels safe, but it guarantees a loss of purchasing power due to inflation. Avoiding market risk exposes you to inflation risk. There is no such thing as a risk-free financial life; you are simply choosing which risk to take.

Managing Risk Without Avoiding Growth

You don’t need to avoid risk; you need to manage it.

Asset Allocation

This is the process of deciding what percentage of your money goes into stocks vs. bonds. A common rule of thumb is “110 minus your age” for the percentage of stocks you should hold. If you are 30, you might hold 80% stocks and 20% bonds. As you age, you shift more toward bonds to preserve capital.

Rebalancing

Over time, your winners will grow and take up a larger piece of your portfolio. If stocks have a great year, your 80/20 portfolio might become 90/10. This makes your portfolio riskier than you intended. Rebalancing involves selling some of the winners (selling high) and buying more of the underperformers (buying low) to get back to your target allocation.

Risk During Market Downturns

Market crashes are inevitable. They are a feature of the system, not a bug.

Volatility vs. Permanent Loss

Volatility is the temporary fluctuation in price. Permanent loss is when an asset goes to zero or when you sell a dropped asset and lock in the loss. If you own a diversified index fund and the market drops 20%, you haven’t lost money—your account value is just temporarily lower. You only lose if you sell.

Emotional Decision-Making

The biggest risk to your portfolio is often the person looking back at you in the mirror. Behavioral finance shows that humans are wired to run from danger (sell when markets drop) and chase pleasure (buy when markets are booming). This is the exact opposite of “buy low, sell high.” Sticking to a long-term plan prevents emotions from destroying your wealth.

Risk Considerations for U.S. Investors

The U.S. financial system offers specific vehicles that change the risk landscape.

Retirement Accounts and Risk

Accounts like 401(k)s and IRAs are designed for long-term investing. Because you are penalized for withdrawing money before age 59½, these accounts force you to have a long time horizon. This structure allows you to take on more risk (more stocks) because you can’t easily panic-sell and spend the cash.

Taxes and Long-Term Planning

Taxes are a guaranteed drag on returns. Holding investments for more than a year qualifies you for long-term capital gains tax rates, which are significantly lower than standard income tax rates. Frequent trading not only increases risk but also increases your tax bill.

Who Should Take More or Less Risk?

Young Investors (20s–30s):

You have the biggest asset of all: time. You can afford to take significant risks because you have decades to recover from downturns. A portfolio heavy in stocks (90–100%) is often recommended to maximize compound growth.

Mid-Career Professionals (40s–50s):

You likely have higher income but also more financial responsibilities (mortgage, kids, college). You still need growth to beat inflation, but you should start introducing some stability. A 70/30 or 60/40 split might be appropriate.

Pre-Retirees and Retirees (60+):

Preservation becomes the priority. You don’t have time to recover from a 50% market drop right before you need to start withdrawing money. However, you cannot go entirely to cash because you might live another 30 years. You need a balanced mix that provides income (bonds/dividends) with some growth to fight inflation.

Conclusion

Risk is the fuel that powers wealth creation. Without it, your money stagnates. By understanding the different flavors of risk—from market fluctuations to the slow erosion of inflation—you can build a strategy that helps you sleep at night while still reaching your financial goals.

Don’t let the fear of short-term loss prevent you from achieving long-term gain. Assess your time horizon, diversify your holdings, and remember that in the world of investing, time is the ultimate risk reducer.

Meta data

Meta title

Understanding Investment Risk: A Guide for US Investors

Meta description

Is the stock market too risky? Learn the difference between volatility and permanent loss, and how to balance risk vs reward for long-term growth.

FAQs – Risk in Long-Term Investments

Is risk bad in long-term investing?

No. Risk is necessary for growth. Without taking on some level of risk, your investments are unlikely to outpace inflation. The goal is to manage risk, not eliminate it.

How much risk should I take?

This depends on your time horizon (when you need the money) and your risk tolerance (how much volatility you can stomach). Generally, the longer you have until you need the money, the more risk you can afford to take.

Can long-term investing be low risk?

Yes, but “low risk” usually means lower returns. Investing in government bonds or high-yield savings accounts is low risk regarding principal loss, but high risk regarding inflation (losing purchasing power).

Does diversification eliminate risk?

Diversification reduces “unsystematic risk” (the risk of a specific company failing), but it cannot eliminate “market risk” (the risk of the whole economy slowing down). It softens the blow but doesn’t remove it entirely.

What is the biggest risk to long-term investors?

For many, the biggest risk is inflation eroding their purchasing power, or their own emotional behavior causing them to sell at the wrong time.